Why a net zero portfolio does not necessarily mean a net zero world

By Helena Wright & Jon Dennis

In the lead up to the UN Climate Conference at COP26, there have been increasing calls for financial institutions to make commitments to net zero greenhouse gas emissions. While the ambition by some has been welcomed, we should not run into the trap of thinking that a net zero emission portfolio, for example by 2050, will necessarily lead us to a safe, carbon-neutral world.

The problem is that transitioning investment portfolios towards net zero greenhouse gas (GHG) emissions by 2050 may not be consistent with a maximum temperature rise of 1.5°C in the real world — the ‘safe’ upper limit of warming as outlined by science. There are several reasons for this which will be explained in this blog, related to how exactly net zero is interpreted and calculated by financial institutions (FIs).

Accounting on net zero

First, it is important to note that these calculations are often derived through carbon accounting which is the process of consistently measuring, tracking and reporting GHGs generated, avoided or removed by an entity over time. More recently these frameworks have been able to measure ‘financed emissions’ that are associated with a financial institutions’ (FIs) investment activity and occur in the value chain of the reporting company or financed activity (also defined as Scope 3 under the GHG protocol).

The most established of these carbon accounting methodologies is the Global Carbon Accounting Standard set out by the Partnership For Carbon Accounting in Financials (PCAF).

Measuring GHG financed emissions through carbon accounting frameworks is a fundamental exercise for FIs, principally because we cannot manage what we cannot measure. However, we must be cautious about some FI commitments that refer to ‘net zero financed emissions’.

Some financial institutions have made statements that they will become net zero but at times, this statement only includes emissions related to their own offices and operations (defined as Scope 1 and 2 emissions). This excludes Scope 3 financed emissions that are considerably larger. For many companies and industries, Scope 3 emissions dominate the overall carbon footprint, and though data is scarce the same is likely to apply to FIs financed emissions.

Other FIs have taken a more ambitious approach to include Scope 3 emissions and to align portfolios with a 1.5°C pathway and the goals of the Paris Agreement. Others still have made commitments to reach net zero emissions by 2050, without detailing a clear pathway to get there. While the terminology is similar, look closer, and these commitments can mean very different things, in terms of timings and real-world emission reductions over the next few decades.

Moreover, carbon accounting is by nature backward-looking (e.g. derived from data that is collected and summed annually) and is not designed to provide information to assess the degree in which a company is or isn’t aligning its business model with a 1.5°C warming trajectory. It is therefore essential that any FI strategy or plan uses carbon accounting in conjunction with other forward-looking approaches that allow for portfolio-wide target setting across asset classes, such as science-based targets for financial institutions.

It is also critical that any carbon accounting reporting does not allow avoided emissions to be taken away from the overall generated emissions of a portfolio. Importantly, this is included in the PCAF methodology and prevents greenwashing claims whereby FIs facilitate continued non-green investment by claiming the emissions and reductions ‘cancel each other out’.

At a global level we cannot merely plant trees while emitting more — that would only keep global emissions constant, not reduce them in the real world.

The infrastructure problem

Another separate issue that must be considered is the time lag between the moment of the investment and the lifetime emissions of infrastructure. This is important because infrastructure makes up around 60% of global greenhouse gas emissions according to the OECD and because certain infrastructure projects have such long lifespans.

Take the example of the energy sector. Thermal power plants can have an operational lifetime of 40 years or more meaning a plant built now could still be around in 2060. In order to limit warming to 1.5°C with “no or limited overshoot”, the IPCC states that global CO2 emissions will need to reach net zero by around 2050 and should show emission cuts by approximately 50% by 2030.

What this actually means is leading FIs need to be pioneers in building and investing in net zero aligned infrastructure and services now, not in later years up to 2050.

Given the timespan of infrastructure investments, FIs should be shifting their investment almost entirely to renewable energy in the near term to align with a 1.5°C pathway. The margin within global carbon budgets is simply too fine to prolong new fossil-dependent infrastructure, unless it is in investments to help transition and eventually phase out that infrastructure.

Globally, a third of oil reserves, half of gas reserves and over 80 per cent of current coal reserves must remain unused from 2010 to 2050 in order to keep warming below 2°C, let alone the more stretching target of 1.5°C. It has been found that reserves in currently operating oil and gas fields alone, even with no coal, would take the world beyond 1.5°C. This indicates that no fossil fuel extraction infrastructure should now be built if we are to meet 1.5°C and Paris Agreement climate goals.

Nevertheless, investment in fossil infrastructure is continuing. Since 2015, global banks have invested $1.9 trillion in fossil fuels.

So, while a net zero commitment might look good at a company or corporate-level, for financial institutions, it might be too good to be true in some cases. There is still a long way to go to align all investment flows towards a 1.5°C world.

The pathway ahead

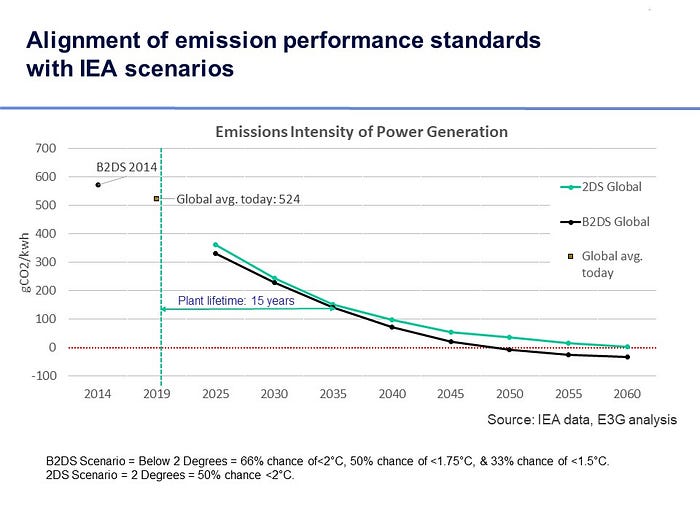

In terms of forward looking approaches the chart below (Source: E3G) reflects that the lifespan of power plants (like gas plants) is at least 15 years. We need to consider how the emission intensity of such assets will impact the grid over this lifespan, and whether this aligns with climate objectives. Under the Below 2 degrees (B2DS) scenario from IEA, new power generation assets built in 2020 need to have an emission intensity of around 150gCO2/kwh in order to stay in line with the B2DS climate scenario in 2035. However, this scenario only gives us a 66% chance of meeting the 2°C goal.

Furthermore, there is opportunity to think differently about how portfolios can be aligned with 1.5°C. Alternative ‘bottom up’ approaches to align with Paris goals at the asset level are being used by some development banks, such as the French Development Agency (AFD). Similarly, banks and investors should now be proactively considering questions such as: what kinds of investments do we need by 2050? What innovation do we need to get there? And how can the finance sector support these changes?

Throughout this journey the importance of consistently used carbon accounting frameworks cannot be overstated, but as indicated above, these approaches must also be combined with best-practice forward-looking methods that encourage short term action towards 1.5°C; reviewed regularly with evolving climate science.

Governments and financial regulators must do more to accelerate the adoption of these practices by setting expectations and ensuring that action is taken by all FIs, not only a select few leaders.

Ultimately, we need all net zero commitments by FIs to be credible, 1.5°C aligned and genuinely transition the wider economy to the sustainable, safe future we are all striving for.

Note: This blog was written in a personal capacity and is not affiliated with any organisation